General Ledger Nebraska

Thus, you need to refer to a related subsidiary ledger to know the details of such a control account. Furthermore, at the end of the accounting period, you close these Ledger Accounts. You do this as a result of balancing the debit and the credit sides of such accounts. Thus, a purchase ledger helps you to keep a track of the purchases your business entity makes.

When you create a journal entry, you must update the general ledger to reflect the changes you’ve made to each account. In the example above, you’d increase your office supplies expense and decrease your cash account by $500. As a result, you and your accounting team will typically consult the general ledger whenever necessary to investigate the details of your business’ activities, transactions, and account balances. With modern accounting software, you may not have a purchase or sales ledger. Instead, they can be marked as a certain type of entry and called up in a search if you want to look at these entries on their own. A ledger is where the most important information necessary to create financial statements is located.

You record the financial transactions under separate account heads in your company’s General Ledger. A General Ledger is a Ledger that contains all the ledger accounts other than sales and purchases accounts. Therefore, you need to prepare various sub-ledgers providing the requisite details to prepare a single ledger termed as General Ledger. General Ledger is a principal book that records all the accounts of your company. Furthermore, all the accounting entries are transferred from the Journal to the Ledger. The general ledger is one of the cornerstones of the double-entry accounting system.

Owner’s equity

If yours is inaccurate, you’ll inevitably have issues with your financial statements. Here’s an example of a journal entry to record the purchase of $500 of office supplies using the funds in your cash account. Sub-ledgers (subsidiary ledgers) within each account provide additional information to support the journal entries in the general ledger. Sub-ledgers are great for accounts that require more details to review the activity. There are several kinds of ledgers that you may use in the course of bookkeeping for your business. Most accounting software will compile some of these ledgers together while still letting you view them independently.

- This ledger is used to record each transaction and uses a trial balance to validate the information.

- A general ledger (GL) is a set of numbered accounts a business uses to keep track of its financial transactions and to prepare financial reports.

- With legacy accounting systems, the chart of account segments are configured at the time of deployment and fixed for the duration of their lifespans.

- The general ledger is a compilation of the ledgers for each account for a business.

- Equity is the difference between the value of the assets and the liabilities of the business.

- Depending on the business’s needs, it typically creates chart of account segments for account, cost center, or department—or possibly even a product or project.

Start making your organization’s general ledger to secure and record all your business’ financial transactions. Generally, it holds all of the financial statements you need to compose other finance documents. It also serves as a source or proof document for company invoices and receipts. Aside from this, the general ledger aids the company in its loan applications, as it provides a complete and detailed document of financial records. It also helps with balancing company checkbooks through a trial balance.

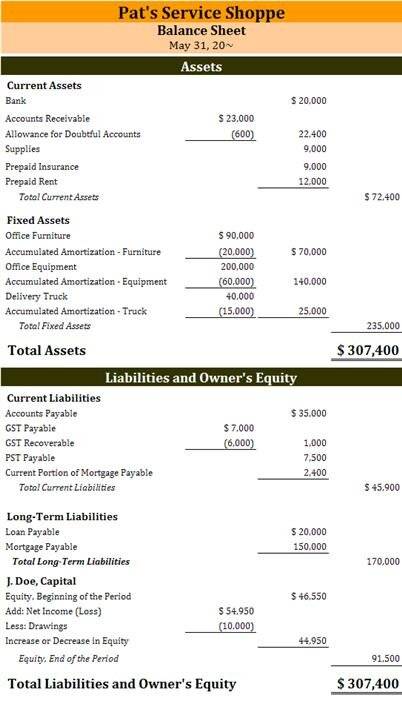

A Balance Sheet Transaction Example

This sub-ledger includes creditors, long-term borrowings, and short-term borrowing. If you have a smaller business, you might have fewer accounts and sub-accounts because you have fewer transactions. Sub-accounts, or sub-ledgers, give you details behind your general ledger entries.

Some general ledger accounts can become summary records and will be referred to as control accounts. In that situation all of the detail that supports the summary amounts in one of the control accounts business vs personal expenses: how to know what’s deductible will be available in a subsidiary ledger. The general ledger must contain a number column where you can indicate the journal transaction ledger corresponding to the general ledger account.

Further, the purchase ledger helps you to know the amount you pay to the creditors as well as the outstanding amount. Besides this, you can refer back to the purchase details in case you need to so in the future. Therefore, a General Ledger helps you to know the ultimate result of all the transactions that take place with regards to specific accounts on a given date.

Accounting 101: How To Master Your Inventory Accounting

Depending on how they are structured by an organization, subledger transactions are generally recorded on a daily, weekly, or monthly basis. Now let’s move on to talk about debits vs. credits and how they work in an accounting system. This includes equity, general reserve, and retained earnings out of the profit. This ledger pertains to the entity’s financial obligation to the outside.

With that, it serves as the company’s primary database for financial records and documents, with other necessary financial papers stemming from the general ledger. Below are the three main components that must be present in your company’s general ledger. In this step, you need to compare the previous accounting periods closing trial balances to the opening balances of the current period ledger accounts. Thus, you need to check the balances for balance sheet accounts like assets, liabilities, and stockholder’s equity. The general ledger is a foundational document in the double-entry accounting system, the most widely accepted modern accounting method. It requires that all financial transactions affect at least two accounts and balance between debits and credits.

These must be relevant to the form of the general ledger you choose to use. The USSGL also provides a statutory format that you can utilize to start your ledger. Guarantee that the table you have consists of assets, liabilities, equities, revenues, and expenses accounts. A general journal is an account where business transactions are recorded as they happen, firsthand, in chronological order before they are posted in their respective accounts in the general ledger. Transferring the financial data from the journal to the ledger is called posting. When posting, the general journal is used to transfer each transaction over to the general ledger.

Subledgers generally contain information about one type of transaction. Posting from general journal to general ledger (or simply posting) is a process in which entries from general journal are periodically transferred to ledger accounts (also known as T-accounts). It is the third step of accounting cycle because business transactions are first analyzed, recorded in the journal and then they are posted to respective ledger accounts in the general ledger. As established, companies rely on general ledgers to ensure that their financial transactions are precise and accurate.

Non-operating or other income accounts

Companies that utilize the double-entry bookkeeping method have a general journal. The general journal is the initial record of financial transactions of an organization. Entries in the general journal are also written chronologically and make it easier for the individual to transfer entries into the general ledger through an account-by-account basis. Guarantee that all necessary information in the general journal must be present in the general ledger.

Small Business Ideas for Anyone Who Wants to Run Their Own Business

Depending on the size of your business and what your business does, you may not need to use all of them. Here are some common types to be aware of and when to use them, beginning with a general ledger of course. A trial balance is an internal report that lists each account name and balance documented within the general ledger. It provides a quick overview of which accounts have credit and debit balances to ensure that the general ledger is balanced faster than combing through every page of the general ledger. A general ledger is the master set of accounts that summarize all transactions occurring within an entity. The general ledger contains all of the accounts currently being used in a chart of accounts, and is sorted by account number.

These accounts provide information that helps you in preparing your business’ financial statements. These financial statements include the income statement and balance sheet. An accounting ledger is the physical or digital record of a company’s finances and can include liabilities, assets, equity, expenses, and revenue. Every business has a variety of expenses and ways of earning income, just as you have different bills and different income streams. You might record these events as they occur in your life in your check register. For a business, all of these financial events, or transactions, must be recorded in their financial books.

Now that you understand what an accounting ledger is and how important it is to keep track of the finances of your small business, you’ll be able to organize and track transactions more easily. If you look at the information that’s recorded in an accounting journal and an accounting ledger, a lot of it would look the same. But there are some differences between how the two records function so it’s important to understand how they work together. As you can see from the image of the general journal in Figure 1, the cash transactions are scattered around on different lines of the journal. This may not seem too bad when there are only four entries, but it becomes a little more difficult to find just the cash entries when there are 54 transactions, or 154!

Rəsmi Saytı 202 Our Lady Of The Pillar College Cauayan – 688

Rəsmi Saytı 202 Our Lady Of The Pillar College Cauayan – 688